Private credit's first real cycle: What it exposes about your operations

Kevin Hsu

It's Tuesday morning, and an analyst already has three names that need attention.

One borrower submitted their quarterly numbers, but the reporting format changed. Their P&L and balance sheet line items don't cleanly match prior reporting periods, and the adjusted EBITDA behind the leverage covenant no longer ties to how the credit agreement defines it. Emails are already going out to the borrower to work out what changed and which add-backs hold up under the agreement.

At the same time, another borrower still hasn't sent theirs. The team has been chasing the financials, and until they arrive there's no read on how much covenant headroom is left, so they're working off last quarter's numbers.

A third borrower did send theirs, but it came in as a dense workbook in its own format, with the add-backs buried across the tabs. Before any of it is usable, the analyst has to re-spread the financials by hand and rebuild the covenant math against a model that's already a quarter out of date.

None of this is unusual.

Most monitoring workflows were built in calmer conditions, where reporting was consistent, and exceptions were manageable. One problem name could be worked through without disrupting everything else.

As private credit moves through its first real cycle at scale, these workflows are being tested under sustained pressure for the first time.

What that exposes isn't only where risk is building. It's how long it takes to get to a portfolio view you can trust, when the data is fragmented and assembled by hand.

These systems weren't designed for this environment. They were built for stability, and are now being tested under stress.

The situations themselves are routine. What's changed is how many land in the same week. Monitoring workflows built for isolated exceptions struggle under that level of simultaneous pressure and eventually break down.

The data problem comes before the credit problem

Covenants only work if the underlying data does. If the figures in the model don't match what the borrower submitted, the covenant test is only as reliable as the reconciliation supporting it. Before the team can act, they need to trust the number. That trust has to be earned position by position, every reporting cycle.

The process is rarely smooth. A borrower submits a compliance certificate with a page of add-backs. The analyst works through each one, accepting some and challenging others, then rebuilds the firm's own adjusted EBITDA. That number becomes the basis for the leverage covenant test, the next IC update, and the quarterly mark. Three outputs, each based on a figure the borrower hasn't agreed to.

On its own, this is manageable. Under pressure, it isn't.

The same process repeats across every borrower, each one with its own format and its own definition of EBITDA. There's no shared structure. The data is scattered across spreadsheets and inboxes, and the logic lives in people's heads.

The weakness becomes obvious when the figures are challenged. An LP asks why revenue is up but leverage is down, or an auditor asks how the mark was derived. To answer, the analyst digs back through the original credit agreement and the compliance certificate definitions, then goes back to the borrower to confirm. It's forensics, and it can take days while new information keeps arriving.

The harder question is who owns the logic. When the covenant model lives in one analyst's spreadsheet and that analyst leaves, the reasoning behind it walks out with them, and the next person rebuilds it from scratch.

This is where the cracks start to show - in everything it takes to get to a number the team can stand behind.

AI doubled, but the workflows underneath it didn't move

These workflows were built for a portfolio where one borrower at a time needed attention. That assumption no longer holds.

Portfolio monitoring was built around a simple reality: every borrower reports differently. No two reporting packages match, and most adjustments come down to judgment. The data got pulled by hand and lived in spreadsheets, one position at a time.

For a long time, that held up. Problems were rare and reporting mostly landed on time, so a stray reconciliation had room to get worked through. The whole approach assumed issues would arrive one at a time.

That's no longer how the work shows up. In a single week, a dozen quarterly packages can land, several of them late, with multiple names already due for covenant review. The workflow still handles things in sequence, even though the portfolio almost never cooperates.

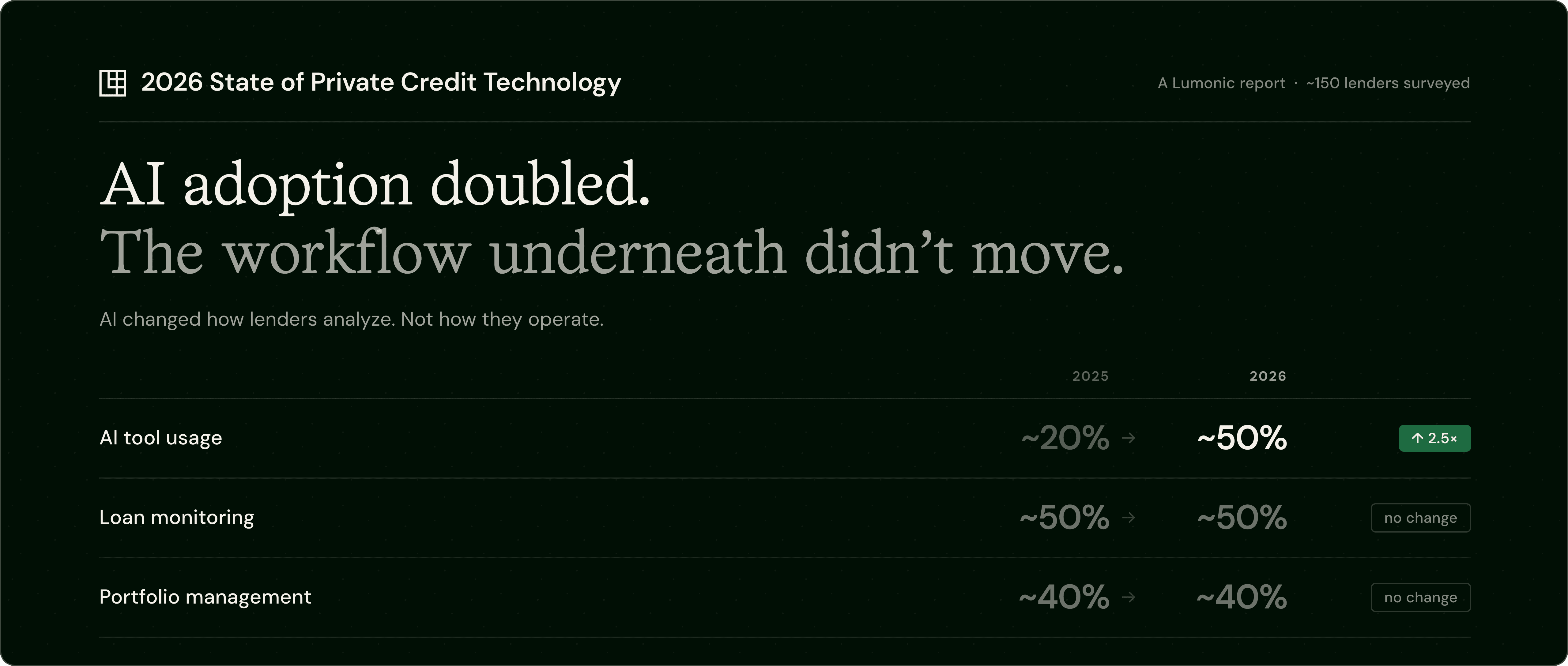

As shown in Lumonic's 2026 State of Private Credit Technology report, AI adoption among lenders more than doubled, from around 20% to roughly 50%. Monitoring and portfolio management adoption didn't move.

AI tools keep multiplying, but the way data gets collected hasn't changed. Teams produce more IC memos and LP updates than ever, all of it still running on the same spreadsheets analysts have reconciled by hand for years. A more polished output on top of the same unreliable inputs.

Analytical tools can only work with what they are given. If the underlying data is delayed or unreliable, the output simply carries those limitations forward.

This becomes most visible at scale. A team running 40 portfolio companies can track covenants in spreadsheets while conditions hold. Under cycle pressure, that starts to give way. Reporting slips and covenant work stacks up just as the first positions start moving toward restructuring.

At that point, the tooling is the constraint. Excel was never built to carry 40 borrowers under stress at once.

Speed to a trusted number is the operational advantage

What separates the firms that hold up under stress is how fast they move from receiving data to acting on it.

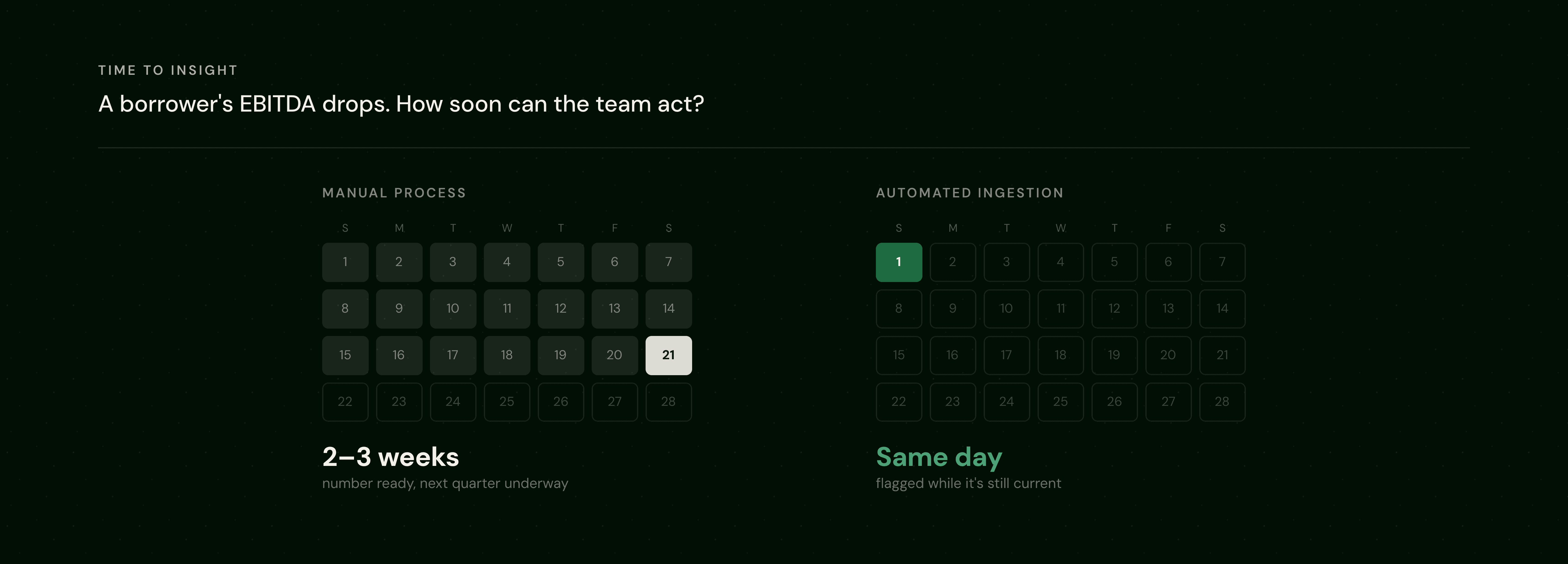

Take a Q1 reporting cycle. A borrower submits financials showing a drop in EBITDA. In a system that works, the number lands and maps against prior quarters the same day, tripping the covenant threshold while the shortfall is still current. The team sees it and acts.

Now compare that to how most teams actually work. The same report lands in an inbox, sits unopened for the better part of a day, then gets extracted and keyed into a spreadsheet by hand. By the time it reaches the team, the data is already a week old.

That delay is the default. A borrower's quarter ends, the package shows up late, and it reaches the portfolio manager two or three weeks after the period closed, with the next quarter already underway. When the data is usable the day it arrives, the gap between what's happening in the portfolio and what the team knows about it collapses.

Traceability is the other piece. A number in a model isn't enough anymore; it has to be defensible. Recent SEC enforcement actions on valuation practices have made that clear. When the question comes, the team has to show where a figure came from and reproduce it on demand, all the way back to the source file.

The firms that handle this well work off live data and one shared set of definitions. The answer is already in the system before anyone asks for it.

Every quarter without the infrastructure is a quarter the early warning arrives too late

Most problems do get caught. The risk is catching them too late to respond.

In more stable conditions, delays in reporting or analysis are frustrating but manageable. Teams can work through a covenant breach or adjust a valuation because there is enough time to reconcile the numbers and rebuild the picture. That room runs out at the wrong end of a cycle.

Recent data shows that distressed exchanges now account for the majority (94%) of defaults. These are the situations where lenders have to move fast, renegotiating or stepping in before performance slides further. Even a short delay in getting to a clear picture narrows the options on the table.

When the data is late or fragmented, the decisions are too. By the time the full picture is clear, the window for a real response has usually closed.

When an LP calls about a borrower's credit position, the answer is already in the system. When the auditor asks how the mark was derived, it traces straight back to the source file. Distressed credits don't wait for the reconciliation to finish. Firms whose data is current and traceable can act on the signal while it still means something. Everyone else is rebuilding the picture.

Lumonic sits at exactly this point in the workflow: portfolio data collected at the source and structured before it reaches an analyst, traceable back to the original filing. Most tools layer AI on top of fragmented inputs. This is the data foundation underneath that makes those tools worth trusting.